Analysis

Taiwan Drone Component Suppliers: Who Makes What

When we published our profile of ten Taiwanese drone manufacturers, we promised a follow-up on the component ecosystem behind them. This is that piece. It matters more than the first one because for most foreign buyers, the realistic near-term opportunity in Taiwan is not a finished airframe. It is the motor, the flight controller, the gimbal, the battery cell, or the composite structure that goes into a platform built somewhere else. And it is at the component layer, not the airframe layer, that the China-free question is actually decided.

Taiwan's drone alliance now counts more than 260 companies, and the MOEA describes a supply chain of 267 firms organized into regional clusters — central Taiwan around Taichung's manufacturing base, a southern validation-and-integration cluster of 45 companies anchored by the Asia UAV AI Innovation Application R&D Center, and even an eastern node. The ministry says more than 20 Taiwanese firms are already inside the US drone supply chain, with overseas order negotiations exceeding NT$10 billion. Only a fraction of these companies ship finished aircraft. The rest are the component and subsystem makers, many of them small and medium enterprises with decades of precision manufacturing behind them and almost no English-language presence. For a buyer at a US or European OEM, they are nearly invisible. This piece maps that layer: who makes what, where Taiwan's depth is real, and — just as important — where it is thin.

The buyer's lens: Section 848 defines the critical list

Before mapping the ecosystem, some context is needed. For US defense buyers, the important components are enumerated in law. Section 848 of the FY2020 NDAA prohibits the Department of Defense from procuring drones manufactured in China or containing critical Chinese components, and the named categories include flight controllers, radios and data transmission devices, cameras, gimbals, ground control systems, operating software, and data storage: essentially every part of a drone that stores or transmits data.

This has two implications. First, "data-touching" components — flight control, comms, optics, positioning — carry the heaviest compliance burden, and that is where a verified non-Chinese source commands the largest premium. Second, there is a known gap: components that do not store or transmit data, such as motors and batteries, have historically received lighter treatment, though newer programs are closing it. For example, the Pentagon's Drone Dominance Program Phase II plans to stop buying systems with motors or batteries from covered countries. Buyers building a durable China-free BOM should treat the whole stack as in scope, because the regulatory perimeter only expands.

Taiwan's government is targeting the same list from the supply side. The NT$44.2 billion (US$1.4 billion) drone industry program running through 2030 explicitly funds core components: chip modules for flight control, communications, and satellite positioning, plus flight and ground control software. The MOEA has committed NT$348 million to drone chip R&D, including dedicated funding for AI image chip modules and low-cost flight control boards that requires domestic chip development or verified applications of non-Chinese silicon. Where the government subsidy is flowing tells you where Taiwan thinks its gaps are and where new suppliers will emerge over the next two to three years.

Propulsion: Taiwan's deepest layer

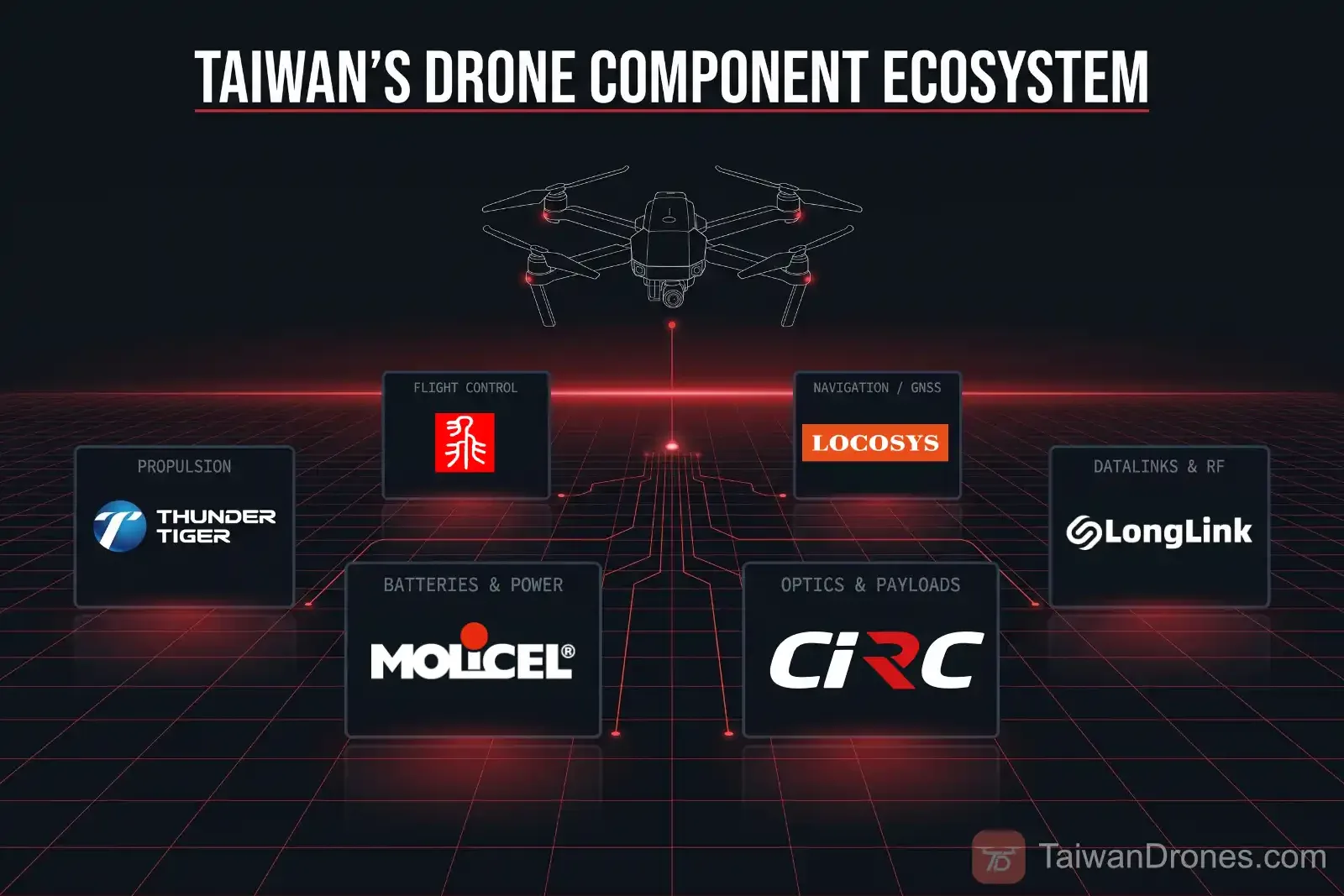

If Taiwan has one component category with genuine, decades-old manufacturing depth, it is motors. The heritage is the hobby industry: Taichung's radio-control aircraft cluster has been winding brushless motors since long before "drone" was a defense procurement term.

Thunder Tiger runs a brushless motor line rated at 40,000 units per month in Taichung and has now carried that capability into its customer's home market. Its Ohio joint venture is a drone motor production line with a planned annual capacity of 60,000 to 120,000 units, placing Taiwanese motor engineering directly inside the US industrial base. Align, also Taichung-based, has built motors alongside its airframes for more than two decades, with a vertically integrated line running from CNC metal processing and carbon fiber components to finished platforms. And the propulsion bench is deeper than the drone-native names: Fukuta Electric & Machinery, an industrial and EV motor manufacturer, now markets a full brushless drone motor range spanning VTOL, FPV, multi-rotor, and heavy-lift classes — a signal that Taiwan's broader electric-motor industry sees the drone market as worth tooling for.

Electronic speed controllers are thinner as a branded Taiwanese category, but the manufacturing base is demonstrably there and international players are already using it. Scorpion Power System, a power-system brand with two decades in high-performance UAV motors and ESCs, states that its ESCs use all-Western components and are manufactured and assembled predominantly in Taiwan specifically to comply with new security regulations. When foreign brands relocate ESC production to Taiwanese SMT lines for compliance reasons, that is the contract-manufacturing layer of this ecosystem working exactly as advertised and it suggests the raw capacity exists for indigenous Taiwanese ESC brands to emerge.

The honest caveat, and it is a significant one: high-performance brushless motors depend on neodymium magnets, and the rare-earth supply chain — mining and processing — remains overwhelmingly Chinese. Taiwanese industry figures acknowledge that manufacturers here still depend on Chinese-sourced rare-earth magnets and germanium. A Taiwanese motor is not automatically a China-free motor at the raw-materials level. Buyers who need magnet-level traceability should ask for it explicitly; suppliers who can document non-Chinese magnet sourcing hold a genuinely scarce credential. We will examine this in detail in our upcoming propulsion deep dive.

Flight control and avionics: indigenous, but SME-scale

Flight control is the most security-sensitive layer of the stack and the hardest to audit. Taiwan has genuine indigenous capability here, but it is concentrated in a small number of companies rather than spread across an industry.

Taiwan UAV is the notable case: the company began as a flight-control systems developer nearly two decades ago before broadening into full VTOL platforms, and reports the complete elimination of China-made parts from its aircraft. Tainan-based Avilon Intelligence develops its entire stack in-house, from flight control to cloud systems, and markets itself on containing no China-made sensitive components or software. Above the private sector sits NCSIST, the state defense research institute, which has told international media it is developing indigenous flight control computers, EO equipment, and radar precisely to reduce reliance on foreign suppliers for military-grade systems.

The structural reality: Taiwan's midstream flight-controller board industry is dominated by SMEs, and scaling it to the volumes implied by current procurement and export projections requires time and capital. That is precisely why the MOEA's low-cost flight control board funding exists. For buyers, the practical takeaway is that Taiwanese flight controllers exist and are flying, but capacity is limited and lead-time questions deserve early attention. And the software layer above the board remains a declared gap: Taiwan's own commercial guide lists drone flight control software among the priority technologies it is seeking from US partners through licensing and co-design, which is why Western autonomy stacks like Auterion's are flying on Taiwanese military drones rather than competing against a domestic equivalent.

One layer deeper sits the silicon itself, and here precision matters more than slogans. A flight controller assembled in Taiwan may carry a microcontroller designed in Europe, fabbed in one country, and packaged in another, sometimes in China. As we examined in our analysis of why "Made in Taiwan" is not always China-free, where a chip is packaged is not where it comes from but a "CHN" mark on a component will still stop a procurement inspection cold. Suppliers who maintain chip-level origin documentation resolve these questions in days; those who don't lose deals to them.

Navigation and positioning: a quiet strength

Satellite positioning is a layer where Taiwan's electronics industry translates directly. Locosys Technology, based in New Taipei City, has manufactured GNSS modules since 2005 and now supplies multi-constellation, dual-frequency GNSS/RTK modules, dual-antenna heading systems, and IMU/AHRS solutions aimed explicitly at UAV and autonomous-system integrators, with IATF 16949-certified production and NDAA-compliance positioning. Its RTK receivers ship in form factors designed for Pixhawk/PX4-based flight stacks, which is exactly where Western OEMs replacing Chinese GPS units go looking. TEDIBOA has made a point of showcasing the company to visiting delegations, a signal of where the alliance believes Taiwan's component story is strongest.

The nuance a careful buyer will check: GNSS module makers, Locosys included, build on chipsets from various vendors, many of them Taiwanese (MediaTek, Airoha), some not, and production footprints can span multiple sites. Module-level origin documentation, not brand nationality, is what decides the compliance question.

Optics and payloads: the Coretronic advantage

Cameras and gimbals sit on the Section 848 critical list, are historically DJI-dominated, and represent one of the highest-margin segments of the stack. Taiwan's strongest card here is Coretronic Intelligent Robotics (CIRC), the drone subsidiary of the Coretronic optical group. CIRC offers ODM/OEM design and manufacturing for gimbal cameras and ground control systems — not just for its own aircraft — and markets the line as NDAA-ready and fully made in Taiwan. Taiwanese industry reporting indicates CIRC shipped more than 3,000 drones in 2025, the largest single-company scale in Taiwan, with Teledyne FLIR reported as a primary customer. If sustained, this is exactly the kind of tier-one Western validation the rest of the ecosystem is chasing.

The parent group's in-house optics capability is the structural point: most drone OEMs must buy their imaging externally, and most of the world's supply is Chinese. A vertically integrated Taiwanese source for EO payloads is a genuine rarity. The thinner end of this layer is thermal. Infrared sensor supply chains (including germanium optics) still route substantially through China; Western thermal cores are subject to US export controls even for Taiwan; and Taiwan's own priority list names infrared cameras among the technologies it is seeking from US partners. Buyers should expect Taiwanese thermal payloads to incorporate foreign sensor cores — FLIR's, most visibly — rather than indigenous ones, for the foreseeable future.

One area worth watching in this layer: Taiwan's camera-module ODM industry. Companies like Ability Enterprise (optical-mechanical imaging ODM/EMS with machine-vision capability) and Altek (imaging chip design plus AI camera ODM, including Qualcomm vision-platform reference designs) built their businesses on consumer and industrial cameras and have not visibly entered the drone payload market but they represent exactly the kind of adjacent, high-volume imaging capacity that CIRC's parent group has already demonstrated can be redirected toward UAV payloads. If the payload demand materializes at scale, this is where the capacity will likely come from.

Batteries and power: a world-class cell maker next door

Here Taiwan holds a component asset that much of the drone world uses without registering its origin. Molicel — E-One Moli Energy, a subsidiary of Taiwan Cement — manufactures the high-discharge cylindrical lithium-ion cells (the P42A, P45B, P50B and successors) that have become default choices for high-performance and long-range drone builds globally. The cells are made in Taiwan, and the company is moving deliberately into the defense-adjacent market: its 2025 partnership with US-based KULR Technology pairs Molicel power cells with American thermal-management systems in battery platforms aimed at the UAS market.

Downstream of the cell, Voltasphere builds battery packs for EVs and unmanned systems, has structured its corporate entities specifically to keep ownership and supply chains clean of China-linked capital, and is scouting US pack-manufacturing locations — while actively connecting smaller Taiwanese component makers with American buyers who don't know they exist.

The power layer extends beyond the airframe. Phihong Technology, a fifty-year-old Taoyuan power-supply group and one of the six firms the Executive Yuan has named to Taiwan's national drone team, anchors the MOEA's eastern cluster with a full-system integration focus and brings a global charging and power-electronics business (including drone chargers) to a segment of the stack, ground power and charging infrastructure, that fleet-scale drone operations will consume in volume.

Batteries illustrate the pattern buyers should internalize about Taiwan: the strength is often upstream of the finished subsystem. Taiwan may not brand the drone battery you buy, but there is a reasonable chance a Taiwanese cell is inside it.

Datalinks, RF, and the ground segment: the thinnest visible layer

We will be direct about this one: RF datalinks are where Taiwan's English-language component story is currently weakest, and the economics explain why. According to DSET, a non-Chinese SDR video transmission chip can cost as much as ten times the price DJI offers, which is the single starkest cost gap anywhere in the China-free BOM. Taiwan's own commercial guide names high-frequency long-range communication modules and military-grade radio transmission among the priority technologies it is seeking from US partners, an official admission that this layer is a gap, not a strength.

The first dedicated entrants are now appearing. LongLink Solutions, a Taipei company founded in 2025, is the most explicit bet on this gap: it builds non-Red FPV communication modules — air units, ground receivers, video and control links — with a documented China-free BOM and Tier-1 Taiwanese EMS partners for volume manufacturing, and was among the startups the MOEA took to Silicon Valley in May 2026 to court the allied drone market. One young company does not make a layer, but a venture-stage firm building exactly the product this section says is missing — video transmission, the single most DJI-locked link in the FPV stack — is the leading indicator that Taiwan's industry is aware of where the gaps are.

Beyond that, the raw RF engineering exists on the island. Integrated OEMs build or integrate their own links. Taiwan UAV lists wireless data and video link modules among its subsystems. Iwavenology, a National Taiwan University spinout, commercialized an RF front-end system-on-chip for wireless positioning and now appears alongside Jet Hand Technology in the government's passive-radar UAS grouping; together with Tron Future's radar work, these companies (which we will cover in the counter-UAS installment) demonstrate that sophisticated indigenous RF capability exists. It simply hasn't broadly productized into export-ready drone datalinks yet. The government is pushing from the same direction: DSET's research confirms the MOEA's subsidy program specifically emphasizes secure communications modules alongside AI vision chips and flight control. Meanwhile the ground segment is developing on its own track: Qisda's display subsidiary Data Image is opening a Taoyuan production line for ruggedized drone controller and console displays, with volume shipments scheduled for Q4 2026.

Still, a foreign OEM looking for an established Taiwanese datalink vendor with published specs and years of export track record will find a short list today. The honest assessment is that this layer is where Taiwan's ecosystem is visibly under construction rather than built.

For buyers: expect datalinks to be the hardest layer to source from Taiwan today, and expect that to change over the program window. For Taiwanese RF companies: the demand signal from Western integrators is real and largely unmet. You are under-marketed relative to nearly every other layer of this stack. If that describes your company, we would like to hear from you.

Structures, composites, and machining: the invisible foundation

The least glamorous layer may be Taiwan's most defensible. Carbon-Based Technology (UAVER) controls composite airframe production that most other OEMs source externally, holds ISO 9100 aerospace certification and NDAA compliance, and has licensed its materials work into the state apparatus. NCSIST has authorized Air Asia to manufacture composite UAV airframes based on Carbon-Based's designs. Beneath the named companies sits the Taichung precision-machining base — CNC shops, carbon fiber layup, injection molding — much of it built serving the hobby, bicycle, and machine-tool industries, now absorbing drone work. Align's in-house line from raw composites to finished platform is the visible example of a capability that exists across dozens of anonymous suppliers.

This is the layer where Taiwan's cost and quality position against non-Chinese alternatives is strongest, and where the directory work we are doing — profiling the companies with no English web presence — matters most.

Where the map has gaps

An honest ecosystem map includes the holes, and there are five that a sourcing team should carry into every Taiwanese supplier conversation.

Raw materials still lead back to China. Rare-earth magnets and germanium remain Chinese-dominated inputs, and Taiwanese manufacturers acknowledge the dependency. "Assembled in Taiwan from a clean BOM" and "China-free to the raw material" are different claims with different verification costs.

The cost gap is real and uneven. Non-Chinese components carry premiums that vary wildly by layer — modest for structures and machining, severe for RF (the 10x SDR chip example above). Buyers pricing a China-free BOM should budget layer by layer, not with a blanket multiplier; suppliers quoting suspiciously close to Shenzhen prices on data-touching components deserve extra scrutiny, not less.

Chip origin is layered. Taiwan's semiconductor strength is real, but drone electronics routinely carry foreign-designed chips with multi-country fab and packaging footprints. Component-level documentation, not country-of-assembly, settles the question.

Not every Taiwanese drone company is what it appears. Industry insiders have described companies rebranding others' products, and in worse cases remanufacturing Chinese products in third countries to pass domestic testing. This is a minority behavior that the serious majority of Taiwan's industry is eager to see policed but it is exactly why per-product-line verification, rather than company-level branding, is the right standard.

Scale is unproven at the top end. Even among friendly buyers the penetration is early: of 61 Ukrainian UAV-related companies surveyed by Taiwanese think tank DSET, seven source components from Taiwan — airframes, battery cells, flight controllers, motors, and microelectronics. Taiwan is a growing but minority supplier even in the most motivated market on earth. The momentum is real, though: DSET counts at least 33 MoUs signed between Taiwanese UAV companies and foreign partners in a single four-month window of 2025, with the US accounting for the largest share. The opportunity is real precisely because it is early.

What this means for sourcing teams

This map produces three practical rules. First, source by layer, not by logo: Taiwan's strength distribution is uneven, and the right strategy pairs deep layers (propulsion, structures, cells, GNSS) sourced today with thin layers (datalinks, thermal cores) monitored for maturation. Second, demand documentation at the component level — chip origin, magnet origin, cell origin — because that is where the compliance risk actually lives, and because the suppliers who can produce it are self-identifying as the serious ones. Third, assume the map is incomplete: the most interesting Taiwanese component makers are SMEs with no English footprint, and finding them requires being on the ground. That is the work we are doing.

This piece is the anchor for a series of category deep dives, built on factory visits and technical interviews with the companies above and others not yet named. Propulsion is first. If your company belongs on this map — especially in RF, thermal imaging, or ESCs — write to us at info@taiwandrones.com.

→ Subscribe to Taiwan Drone Weekly for the series as it publishes: taiwandrones.com/subscribe

→ Suppliers: contact us at info@taiwandrones.com

Disclaimer: This article is provided for informational purposes based on publicly available information as of July 2026. Company capabilities and compliance statuses described here reflect public statements and reporting, not independent verification by TaiwanDrones.com unless explicitly stated. Buyers should conduct their own due diligence and consult qualified export-control and trade compliance counsel for their specific situation.